The Corporate Sustainability Reporting Directive - CSRD

On January 5, 2023, the Corporate Sustainability Reporting Directive (CSRD) came into effect, marking a significant update aimed at enhancing the disclosure requirements concerning social and environmental aspects for companies. This directive broadens the scope to include a wider array of large companies and listed SMEs, mandating them to report on sustainability matters. Additionally, non-EU companies will need to report if their EU market revenue exceeds EUR 150 million.

These updated regulations are designed to ensure that investors and stakeholders have access to comprehensive information to evaluate companies' impacts on society and the environment. Furthermore, they enable investors to assess financial risks and opportunities related to climate change and other sustainability factors. Harmonizing the information requirements will also lead to reduced reporting costs for companies in the medium to long term.

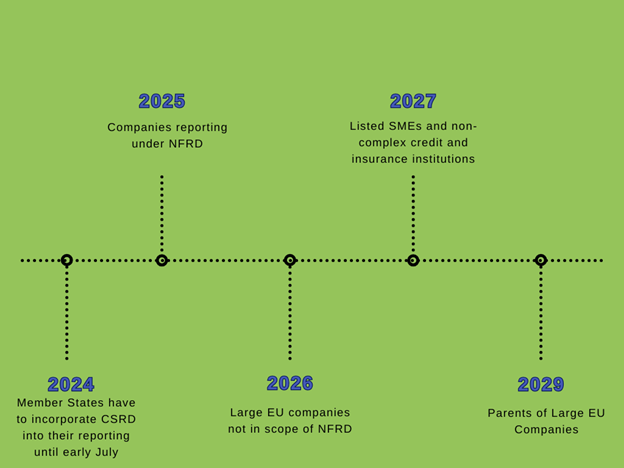

Under the CSRD, companies falling within its scope will report based on European Sustainability Reporting Standards (ESRS). These standards, developed in draft form by the EFRAG (European Financial Reporting Advisory Group), now known as an independent entity, gather input from various stakeholders. Furthermore, the CSRD mandates assurance on reported sustainability information and establishes a framework for the digital taxonomy of sustainability data. The implementation of the new CSRD legislation, effective from January 1, 2024, marks a pivotal moment in standardizing non-financial reporting. It mandates approximately 50,000 large companies and listed SMEs operating within the EU to report on their climate impact and commence regular reporting starting in 2025, reflecting the financial year 2024.

This obligation extends to EU companies meeting two of the following criteria (€40 million in net revenue, €20 million in assets, 250 or more employees), as well as non-EU entities with significant operations in the EU, including a physical presence. Non-EU companies with EU net turnover exceeding €150 million over the last two consecutive years, possessing at least one large or EU-listed subsidiary or branch generating a minimum EU revenue of €40 million. The CSRD's extraterritorial reach extends to companies headquartered outside the EU but operating within its borders. Consequently, such entities may find themselves obliged to adhere to both EU regulations and those stipulated by their home jurisdictions. While the CSRD incorporates a mechanism for the Commission to assess the equivalence of third-country issuers, the specifics of the Commission's approach in this regard remain unclear.

Furthermore, the disclosed information is subject to a double materiality principle. This means that companies must not only comprehend the impact of their operations on sustainability issues but also grasp how sustainability factors influence their business development, performance, and positioning.

Companies falling under the jurisdiction of the CSRD will be obligated to disclose sustainability information utilizing the European Sustainability Reporting Standards (ESRS), developed by the European Financial Reporting Advisory Group (EFRAG) at the request of the European Commission.

EFRAG has structured the ESRS into three distinct categories, each complementing and interrelating with the others:

- Cross-cutting standards: establishing general requirements for companies to adhere to when preparing and presenting sustainability-related information; they will be applicable to all companies, irrespective of the sector they operate in, and cover a wide range of sustainability topics.

- Topical standards: focus on specific sustainability subjects, disclosing sustainability impacts, risks, and opportunities from a sector-agnostic standpoint.

- Sector-specific standards: disclosing requirements pertaining to sustainability impacts, risks, and opportunities that hold significance for all entities operating within a particular sector.

Timeline of the CSRD

In addition, the CSRD outlines the sustainability data that companies must incorporate into their sustainability reports. This entails furnishing both qualitative and quantitative information, surrounding forward-looking and retrospective perspectives, and spanning short-, medium-, and long-term outlooks. Companies are tasked with disclosing environmental and social risk factors to aid stakeholders such as investors, policymakers, and consumers in assessing their performance. Compliance with these new provisions necessitates a deeper understanding beyond mere regulatory adherence. It urges companies to reevaluate their strategies, governance, operations, and data management practices. Specifically, companies within the scope must:

- Formulate decarbonization strategies and transition plans, conduct scenario analyses, and calculate their carbon footprint.

- Ensure alignment between reporting and corporate strategy, ensuring that targets are both credible and effectively communicated to external audiences.

- Enhance risk management processes and governance structures.

- Establish due diligence mechanisms to identify and mitigate risks within their supply chains.

The Corporate Sustainability Reporting Directive represents a pivotal advancement in corporate transparency and accountability regarding sustainability. By mandating standardized reporting on environmental, social, and governance (ESG) factors, the CSRD equips investors, stakeholders, and consumers with consistent and comparable information to inform decision-making. Emphasizing digitalization, it encourages efficient data dissemination and stakeholder engagement. Ultimately, the CSRD opens a new era where businesses prioritize transparency, accountability, and long-term value creation, fostering a more sustainable and responsible corporate landscape for the future.

For more information, feel free to contact Global Connect Admin - info@Globalconnectadmin.com